Why Capital Markets, Not Policy, Will Decide the Future of Critical Minerals

This is an anchor essay. I’ll be building on this thesis over the coming months.

The global race for critical minerals is often framed as a policy challenge. Governments in the West have responded with strategies, regulations, subsidies, and declarations of strategic intent. Yet, despite unprecedented political attention, the West (and Europe in particular) continues to struggle to secure reliable, scalable, and sovereign supply chains for the materials that underpin the energy transition, advanced manufacturing, and national security. This failure is not the result of insufficient ambition or inadequate regulation. It reflects a more profound misunderstanding of what actually determines outcomes in capital-intensive industries. Despite the illusion of control, policies do not secure critical minerals. These minerals are secured by capital.

Supply chains start with mines at the upstream part.

These mines are built, expanded, and integrated into supply chains not because a government declares them strategic, but because capital is mobilised at scale, deployed patiently, and recycled efficiently. As a result, it is ownership, balance sheets, liquidity, and execution capacity that determine who controls the supply of these critical minerals. Policy can influence the environment in which capital operates, but it will never be a substitute for capital itself.

The uncomfortable truth is that the players who dominate some of the critical mineral chains today (such as China and Russia) did not achieve this solely by drafting better policy documents. They also ensured (and often forced) their capital markets to align with long-term industrial objectives, accepting risk where others hesitated and ensuring assets remained funded through cycles. In contrast, much of the Western approach has prioritised regulation over ownership, subsidies over liquidity, and intent over execution; the result is a widening gap between strategic ambition and industrial reality. The future of critical minerals will not be decided in ministries or conferences. It will be decided in capital markets, by who can raise financing, who can structure it intelligently and retain control, and who can scale these assets over time. Everything else is secondary.

Western approaches have led to policy illusion. Policy always plays a key role in shaping commodity markets, but it has increasingly been treated as a proxy for action rather than as a facilitator. In the case of critical minerals, this has created the illusion that the right combination of regulation, incentives, and strategic language could, on its own, deliver secure supply chains. In the West, policies move at the speed of electoral cycles, consultations, and compromise. Mining projects and processing infrastructure, in contrast, operate on timelines measured in decades. The mismatch is structural, not accidental. However, it is no longer accurate to treat “the West” as a single model.

We can point to three distinct approaches that have emerged over the past decade. These three models (the United States, Australia, and Europe) each reveal distinct relationships among policy, capital markets, and execution, which are delivering varied results. For the United States, policy has been used as a catalyst for capital rather than a substitute for it. This shift, which began under the Biden administration, has accelerated under the Trump administration through a sharper alignment between industrial objectives, national security, and capital markets. While imperfect, the direction is clear: crowd in private capital, de-risk scale, and anchor assets within deep, liquid public markets.

Australia offers a different but instructive model. It has built one of the world’s most successful mining sectors not through heavy industrial policy, but through functional capital markets that understand resource risk. For decades, Australian markets have funded projects from the very early stages of exploration through production. The limitation has not been capital formation, but capital retention and further expansion of the supply chain, particularly further downstream. Europe, by contrast, remains largely in a phase of conceptual alignment rather than operational execution. Its policy frameworks are comprehensive and values-driven, but capital-light. Markets are fragmented, liquidity is shallow, and development-stage risk is often treated as a liability rather than a necessity. Across all three approaches, the lesson is consistent. Where policy complements capital markets, projects advance (Australia, USA). Where policy attempts to replace capital, like in Europe, execution falters. Subsidies and grants may help at the margins, but capital that cannot scale and exit does not stay. Until this distinction is fully internalised, Europe-based critical minerals strategies will continue to look robust on paper but deliver uneven results in practice.

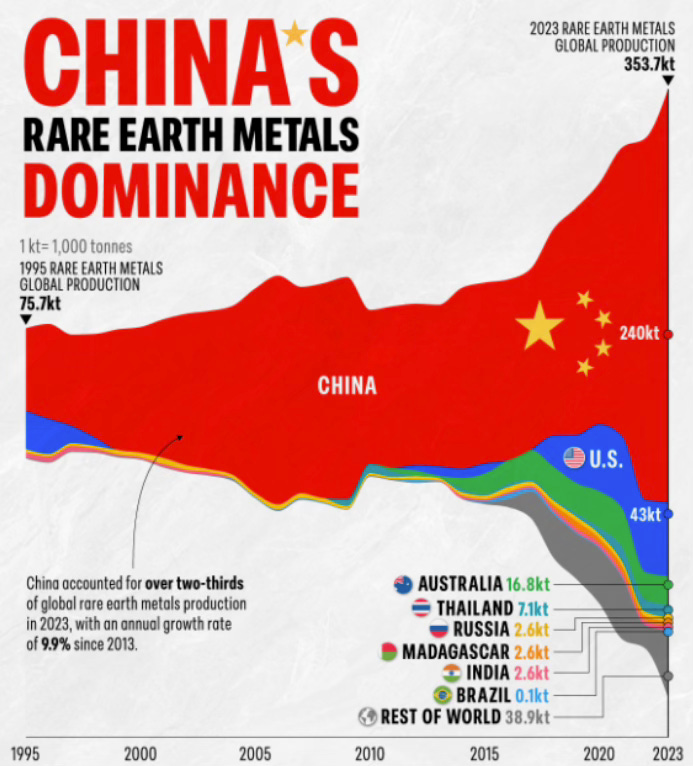

China’s dominance in critical minerals is usually attributed to state planning, subsidies, or regulatory asymmetry. These explanations are somewhat incomplete because they omit the capital factor. China did not achieve its dominant position in critical minerals supply chains solely through policy. It won it through the deployment of capital, in early stages and at scale. More importantly, this capital was deployed with a tolerance for time and loss that was politically, economically, and socially unacceptable in the West.

From the outset, China treated critical minerals as an industrial system to be built end-to-end. Capital flowed across mining, processing, refining, and downstream integration. Losses in one segment were absorbed to secure dominance in another. Assets were funded and supported through downturns rather than abandoned. Ownership was central. Rather than relying solely on regulation to ensure access, China embedded its financial institutions directly into the physical and economic infrastructure of supply chains. As a result, control and capital went hand in hand. Chinese public markets reinforced this strategy. Listings were used to recycle capital once scale was achieved, freeing balance sheets for redeployment elsewhere. Liquidity was a feature, instead of an afterthought. The result we see now is that China has a vertically integrated ecosystem that is difficult to displace, because it has been capitalised over decades, through good and bad times. In addition, new ownership and technology transfer regulations are now locking out external participants. The key lesson is not ideological. The first step of China was not to out-regulate competitors; it was to out-capitalise them. Any serious response must begin with this reality.

Assets Without Capital, A Western Paradox:

Another persistent misconception in the critical minerals debate is that the West is losing because it lacks resources. In reality, the opposite is true. Across North America, Australia, and Europe, the West controls world-class geological assets, advanced technical expertise, robust legal systems, and deep pools of institutional capital. And yet, it consistently struggles to convert these advantages into operating, scaled, and resilient supply chains.

We call this the Western paradox: an abundance of assets, but a scarcity of capital deployment at the point where it matters most. The problem is not the absence of money. Globally, capital has rarely been more plentiful. The problem lies in how long-cycle, capital-intensive mining projects intersect with modern Western capital markets, regulatory processes, ideology, and public sentiment, particularly in Europe. Projects are delayed, diluted, or abandoned not because they are uneconomic in the long run, but because the environment in which they are expected to develop is structurally misaligned.

Public markets are generally hostile to development-stage assets. Long timelines, construction risk, and commodity price volatility are penalised rather than understood. Private capital, meanwhile, requires credible exit pathways that are often unavailable. In the absence of liquidity, ownership fragments, and strategic assets are sold prematurely or consolidated elsewhere. Liquidity, therefore, becomes the missing link. Across jurisdictions and capital-market regimes, the same pattern repeats itself. Experienced boards identify substantial assets and assemble capable technical teams while ensuring asset development is carried out in accordance with policy support. Yet, capital never arrives, or is too late, in insufficient size, or under structures that prioritise short-term survival over long-term control. Projects stall not because the assets are weak, but because the route from capital to execution is poorly designed.

In Europe, particularly, this capital challenge has been compounded by an increasingly polarised public debate over mining itself. A vocal cohort of what might best be described as armchair environmentalists has opposed almost any form of domestic mining activity, often without engaging thoughtfully with the trade-offs involved. The result has been a public discourse that treats extraction as inherently incompatible with environmental responsibility, while ignoring the reality that demand does not disappear simply because production is displaced elsewhere. This dynamic creates a quiet but damaging contradiction. Mining is resisted domestically on environmental grounds, while the same materials are imported from jurisdictions with weaker standards, less transparency, and poorer oversight.

Environmental risk is not eliminated; it is merely outsourced. We are not arguing for lowering standards. On the contrary, high environmental and social standards are a comparative advantage for Western jurisdictions. But standards must be paired with honest education and credible supervision. Governments have a responsibility to explain not only the risks of mining, but also its benefits (economic, strategic, and environmental) when conducted properly. A mature benefit–risk assessment recognises that responsible domestic production often represents a lower overall environmental cost than reliance on opaque foreign supply chains.

Absent this balance, capital hesitates. Investors are reluctant to commit to projects exposed to prolonged permitting risk, social opposition, and shifting political signals. The result is predictable: capital flows elsewhere, ownership is lost, and strategic dependence deepens. This approach is not a failure of environmental values. It is a failure to reconcile those values with industrial reality. Until Europe, and the West more broadly, aligns public understanding, regulatory supervision, and capital-market design, it will continue to possess the right assets while struggling to finance, own, and scale them responsibly.

Capital Markets and Ownership are strategic to critical minerals supply chains. Capital markets are often treated as neutral financial plumbing. In reality, they are strategic infrastructure. They price risk, discipline management, enable scale, and provide liquidity. Without these functions, capital becomes episodic, ownership becomes fragile, and long-cycle investments are forced to align with short-cycle expectations.

Where capital markets are deep and aligned, assets move from development to scale. Where they are fragmented or shallow, even strategic projects struggle. This distinction explains much of the divergence between the U.S., Australia, and Europe. It also explains why policy alone cannot compensate for a weak capital-market infrastructure. Industrial strategies that ignore capital markets design are incomplete by definition.

Regulation shapes behaviour, but ownership determines outcomes. In critical minerals supply chains, supply reliability matters more than marginal price. What makes them strategic is the leverage they have on the downstream part of the economy, particularly in energy transition, technological, and defense sectors. In such contexts, the ability to direct investment, prioritise offtake, and reinvest through cycles outweighs any regulatory safeguard. The Western instinct has been to rely on rules to secure access. In practice, this produces permitted and compliant assets, but not necessarily controlled ones.

The introduction of FDI rules can prevent undesirable ownership patterns, but it can also create situations in which key assets become stranded. Whereas regulation is designed to police outcomes externally, ownership aligns incentives internally. What is required is an approach of strategic openness, which enforces alignment of capital and reciprocal ownership; in the end, those who dominate supply chains do so because they own them.

But what does that mean in practice? If capital markets are decisive, then market readiness must be foundational, not optional. Projects must be designed with capital pathways in mind from the outset. Capital structures should anticipate scale, refinancing, and liquidity. Governments should prioritise bankability over symbolism. Management teams must think like capital allocators as much as operators. Not all listing venues are equal. Depth, liquidity, and alignment matter more than geography. The projects that succeed will not be those with the most substantial policy endorsements, but those financed, governed, and scaled with capital markets in mind from day one.

Critical minerals strategies are initially evaluated by their ambition. But the outcomes are determined by execution. Policy matters, but it does not build mines. Regulation matters, but it does not scale supply chains. Capital does.

Where capital markets function as strategic infrastructure, assets are built and retained. Where they do not, strategies remain aspirational. Supply security cannot be regulated into existence. It must be financed, owned, and executed into existence.

In the end, supply chains follow capital flows. That is the deciding variable.

Daniel Mamadou-Blanco

Singapore, 31 December 2025